bankruptcy terms

How Do You File Bankruptcy? A Step-by-Step Legal Guide

How Do You File Bankruptcy and What Should You Expect? If you’re asking how do you file bankruptcy, you’re not

Error: Contact form not found.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

If you’re asking how do you file bankruptcy, you’re not alone. Thousands of Americans consider bankruptcy each year to relieve overwhelming debt. Understanding how the process works can help you make smart choices and avoid costly mistakes.

Filing for bankruptcy may seem intimidating, but with the right information and legal guidance, it can be a straightforward path to financial relief. Below is a clear step-by-step guide to help you navigate the process and understand what to expect.

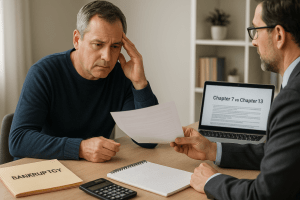

This is often called “liquidation bankruptcy.” It involves selling non-exempt assets to pay off debts. Many unsecured debts—such as credit cards, personal loans, and medical bills—may be discharged, depending on the circumstances. The process is generally shorter than other chapters and often lasts approximately 3 to 6 months, depending on the case.

This is known as a “reorganization bankruptcy.” It allows you to keep your assets and repay some or all of your debts over a 3- to 5-year plan. If you have regular income and want to prevent foreclosure, Chapter 13 may be the better route.

When considering how do you file bankruptcy, choosing the right chapter is critical. Each option has different requirements and outcomes.

Before you file, you must complete a credit counseling course from an agency approved by the U.S. Trustee Program. This course helps evaluate if bankruptcy is your best option and must be completed within 180 days before filing.

Organize documents such as:

Having accurate and complete records is essential when determining how do you file bankruptcy properly.

You must complete and file the bankruptcy petition along with multiple financial disclosure forms in your local federal bankruptcy court. Once filed, an automatic stay generally goes into effect, which may pause certain collection activities, lawsuits, or wage garnishments, subject to court rules and exceptions.

About a month after filing, you’ll attend a court-supervised meeting, often called a “341 meeting.” A bankruptcy trustee will ask questions about your financial situation. While creditors are allowed to attend, they usually don’t.

Before receiving a discharge, you’ll need to complete a second course focused on financial management. This step is mandatory to finalize your bankruptcy case.

If you’re filing Chapter 7, most of your debts will be discharged within a few months. If you filed Chapter 13, your repayment plan must be completed before discharge. Either way, this step typically concludes the bankruptcy case and allows individuals to begin addressing their financial situation moving forward.

Once your case is discharged, you are no longer legally required to pay discharged debts. While bankruptcy does impact your credit, it may provide an opportunity to reassess finances and work toward rebuilding over time Some individuals are able to access new forms of credit over time, depending on their financial circumstances and lender requirements.

You’ll also want to monitor your credit report, follow a strict budget, and avoid taking on new debt too quickly. Learning how do you file bankruptcy also means preparing for the financial steps that follow it.

If you’re unsure where to begin, resources from reputable legal networks and bankruptcy lead providers can help connect you with experienced professionals.

Understanding how do you file bankruptcy is the first step toward financial relief. By following the correct legal process—from choosing the right chapter to completing required courses and court filings—you may be able to address ongoing collection activity and begin planning next financial steps. Whether you’re considering Chapter 7 for a fresh start or Chapter 13 for structured repayment, informed choices and legal guidance can help individuals better understand their options and the process.

Still unsure how do you file bankruptcy or which chapter is right for your situation? Get the support you need to move forward with confidence. Start with a free evaluation from bankruptcy attorneys to discuss your situation and explore available legal options.

Chapter 7 takes about 3–6 months, while Chapter 13 repayment plans last 3–5 years.

Yes, depending on your state’s exemption laws and whether you’re filing Chapter 13 or Chapter 7 with equity protection.

It eliminates most unsecured debts. Some obligations like student loans, child support, and recent taxes typically remain.

Yes, joint filing is allowed and can help if both parties share liability for debts.

Yes. While it remains on your credit report for up to 10 years, many people start rebuilding credit within 12 months.

Attorney Advertising. This site is a legal marketing service and does not provide legal advice. Submitting information does not create an attorney-client relationship. Results are not guaranteed.

How Do You File Bankruptcy and What Should You Expect? If you’re asking how do you file bankruptcy, you’re not

| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |